AP Physics 2 Premium, 2024 - Microeconomics Practice Test

1. Which of the following is NOT a characteristic of perfectly competitive industry?

(A) Free entry into the industry

(B) Product differentiation

(C) Perfectly elastic demand curve for firms

(D) Homogeneous products

(E) Many sellers and many buyers

2. Which of the following is a characteristic of monopolistic competition in the long run?

(A) Strong barriers to entry

(B) Homogeneous products

(C) Zero economic profits

(D) Minimum average total cost equals price

(E) Allocative efficiency

3. Which of the following is (are) characteristic of an oligopoly?

I.Formidable barriers to entry

II.Mutual interdependence

III.Relatively few sellers

(A) I only

(B) II only

(C) III only

(D) I and III only

(E) I, II, and III

4.Which of the following is a characteristic of a monopoly?

(A) A price that is always in the elastic range of the demand curve

(B) Price equal to marginal revenue

(C) Perfectly elastic demand curve

(D) Low barriers to entry

(E) Zero economic profits

5. Compared to perfect competition in long-run equilibrium, a monopoly has

(A) more choices of products for consumers.

(B) allocative efficiency.

(C) lower prices.

(D) a price less than marginal cost.

(E) a price greater than marginal cost.

6. With the presence of a negative externality, which of the following would correct the externality?

(A) A per-unit subsidy

(B) A per-unit tax

(C) A lower price

(D) A higher level of output

(E) A government-created task force

7. With the presence of a positive externality, which of the following would correct the externality?

(A) A per-unit subsidy

(B) A per-unit tax

(C) A higher price

(D) A lower level of output

(E) A government-created task force

8. Which of the following is true regarding externalities?

(A) Marginal social cost = marginal private cost + marginal social benefit.

(B) Marginal social benefit = marginal private benefit + marginal social cost.

(C) Marginal social cost = marginal private cost + marginal external benefit.

(D) Marginal social cost = marginal private cost + marginal external cost.

(E) Quantity of externality = marginal private costs.

9. Which of the following is true?

(A) Average total cost = total fixed costs divided by the number of units produced.

(B) Average total cost = average variable costs divided by the total number of units produced.

(C) Average total cost = average variable cost plus marginal cost.

(D) Average total cost = average variable cost plus average fixed cost.

(E) All of the above.

10. Which of the following is true about the relationship of the average total cost (ATC) curve and the marginal cost (MC) curve?

(A) ATC and MC are always equal.

(B) ATC and MC are never equal.

(C) The ATC curve intersects the MC curve at the minimum point of the MC curve.

(D) The MC curve intersects the ATC curve at the minimum point of the ATC curve.

(E) The MC curve intersects the ATC curve at the maximum point of the ATC curve.

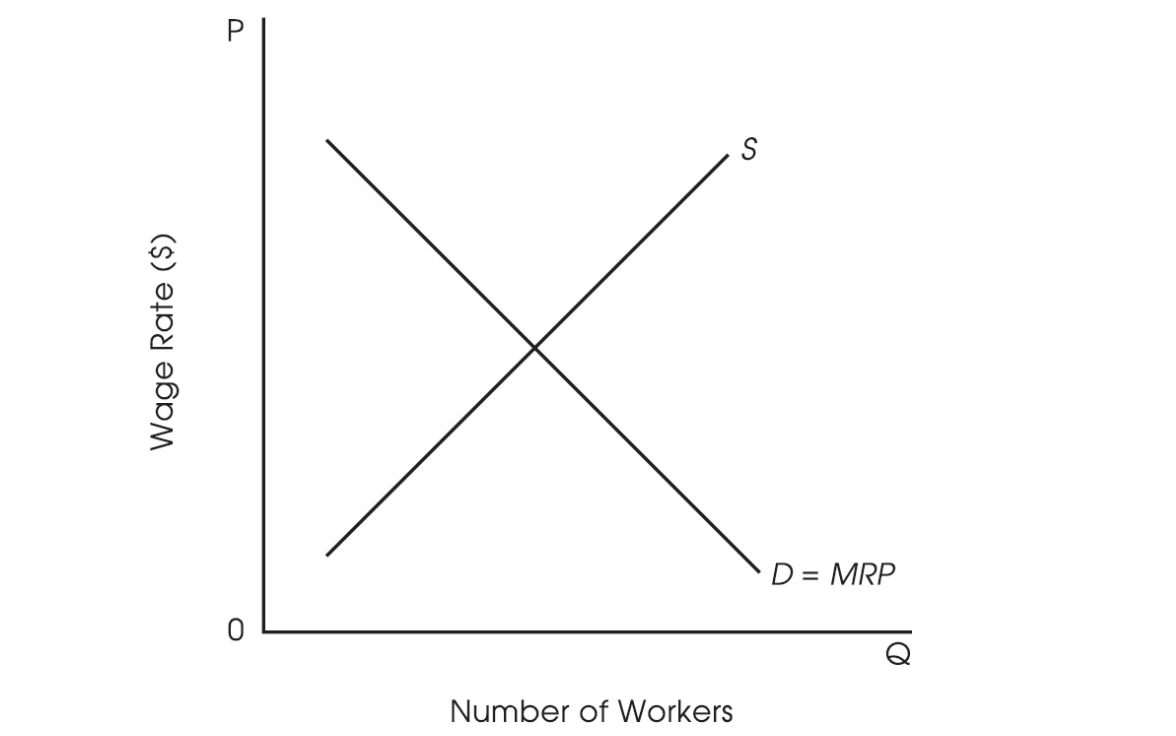

Question 11 is based on the figure below.

11. Which of the following will happen when a new computerized system for a firm increases the marginal productivity of its workers?

(A) The marginal revenue product curve will shift to the left, which will cause the wage rate to decrease.

(B) The supply curve will shift to the right, causing the wage rate to decrease.

(C) The marginal revenue product curve will shift to the right, causing the wage rate to increase.

(D) The supply curve will shift to the left, causing the wage rate to increase.

(E) The marginal revenue product curve will shift to the right and the supply curve will shift to the left, leaving the wage rate unchanged.

12. Which of the following is true about an effective price floor?

(A) It is used to correct government policy.

(B) It is used when the equilibrium price is too high.

(C) It will be located above the equilibrium price.

(D) It will be located below the equilibrium price.

(E) It is when the stock market has closed at a new low.

13. Which of the following is true about an effective price ceiling?

(A) It is used to correct government policy.

(B) It is used when equilibrium prices are too low.

(C) It will be located above the equilibrium price.

(D) It will be located below the equilibrium price.

(E) It is when the stock market has closed at a new high.

14. Which of the following situations best exemplifies the concept of consumer surplus?

(A) It refers to a consumer who no longer has any outstanding debts.

(B) The federal government has taken in more revenue than it has paid out in expenditures.

(C) A consumer does not buy a pizza as it costs more than the highest price she is willing to pay.

(D) A consumer pays less for a pizza than the highest price she is willing to pay.

(E) A consumer buys a pizza for the exact highest price she is willing to pay.

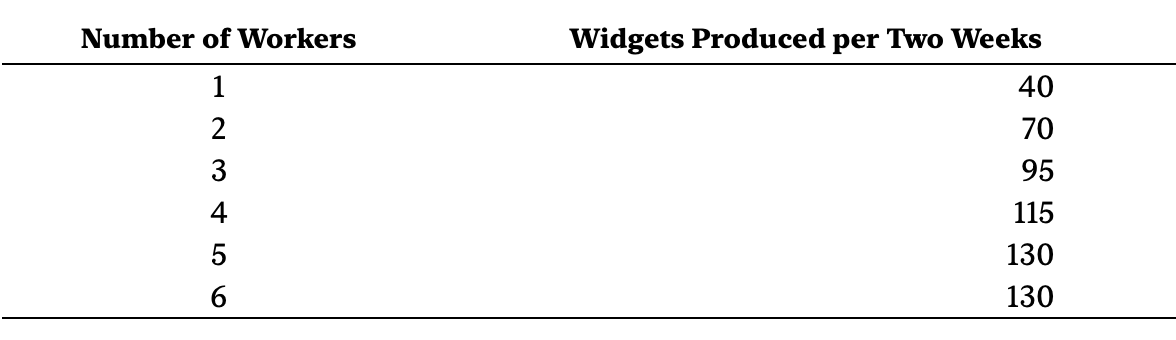

15. Given the data in the table above and knowing that workers are paid $1,250 every two weeks and that widgets are sold to retailers at $50, how many workers would be hired?

(A) Two

(B) Three

(C) Four

(D) Five

(E) Six

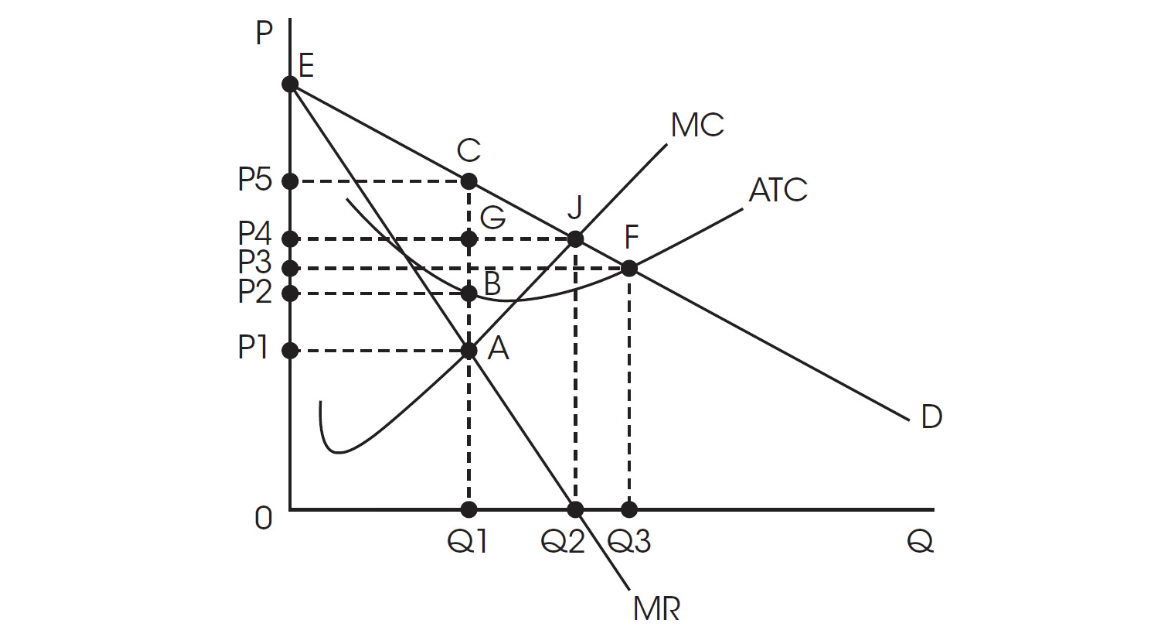

Questions 16–19 are based on the monopoly graph below.

16. An unregulated, profit-maximizing monopoly will produce at which quantity and price?

(A) Q1, P5

(B) Q1, P2

(C) Q1, P1

(D) Q2, P4

(E) Q3, P3

17. If this monopoly were regulated as a natural monopoly and ordered to produce at the socially optimal quantity, what would be the quantity and price?

(A) Q1, P5

(B) Q1, P2

(C) Q1, P1

(D) Q2, P4

(E) Q3, P3

18. What is the area of economic profit if this was an unregulated, profit-maximizing monopoly?

(A) 0, P2, B, Q1

(B) 0, P5, C, Q1

(C) P2, P5, C, B

(D) P1, P5, C, A

(E) 0, P1, A, Q1

19. If a lump-sum tax were now placed on this unregulated monopoly, what would happen to the new profit-maximizing quantity and price?

(A) Price and quantity would remain unchanged

(B) Price would increase and quantity would decrease

(C) Price would decrease and quantity would decrease

(D) Price would decrease and quantity would increase

(E) Price would increase and quantity would increase

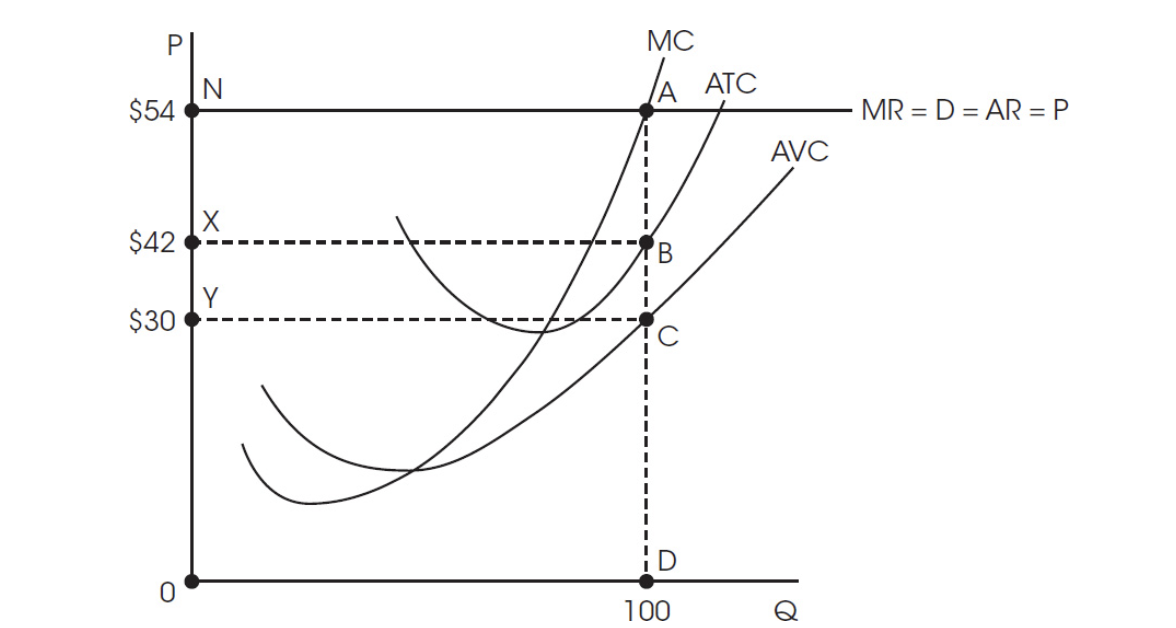

Questions 20–22 are based on the perfectly competitive market depicted below.

20. At a market price of $54, the area of profits or losses is

(A) 0, Y, C, D

(B) 0, X, B, C

(C) X, N, A, B

(D) Y, X, B, C

(E) 0, N, A, D

21. Based on the graph, what is the total fixed cost at the profit-maximizing quantity?

(A) $54

(B) $1,200

(C) $2,400

(D) $3,000

(E) $5,400

22. What will happen to the number of firms in the long run in this industry based on the profit conditions in this perfectly competitive firm?

(A) The number of firms will increase as the existence of economic profits attracts more firms.

(B) The number of firms will decrease as the existence of economic profits attracts fewer firms.

(C) The number of firms will decrease as the existence of economic losses causes firms to leave

(D) The number of firms will increase as the existence of economic losses attracts more firms.

(E) The number of firms will remain unchanged as all the profits in the industry are gone.

23. If a 10% increase in the price of good A leads to a 20% decrease in the quantity demanded of good B, then

(A) the cross-price elasticity is 0.5 and the goods are complements.

(B) the cross-price elasticity is -2 and the goods are complements.

(C) the cross-price elasticity is 2 and the goods are complements.

(D) the income elasticity is 2 and the goods are inferior.

(E) the income elasticity is 0.5 and the goods are normal.

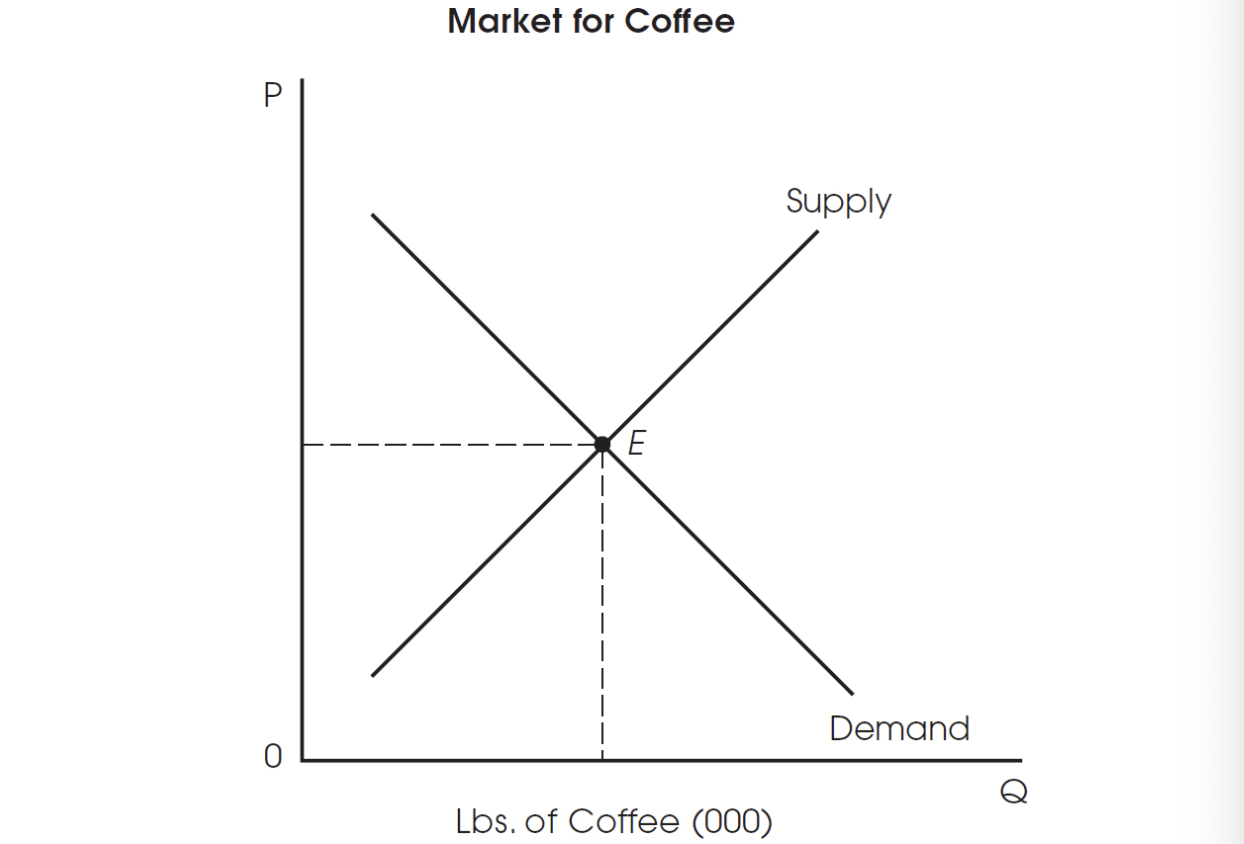

Questions 25–28 are based on the figure below.

25. If the demand for coffee increases and at the same time increases in productivity lower production costs, what would happen to the new price and quantity?

26. If the government provides a subsidy to the producers of coffee, which of the following will occur?

(A) A shift to the left of the supply curve

(B) A shift to the left of the demand curve

(C) A move along the supply curve to the right

(D) A shift to the right of the demand curve

(E) A shift to the right of the supply curve

27. If the producers of coffee have to pay an increase in wages and fringe benefits to their workers, which of the following is correct?

(A) A shift to the left of the supply curve

(B) A shift to the left of the demand curve

(C) A move along the supply curve to the right

(D) A shift to the right of the demand curve

(E) A shift to the right of the supply curve

28. If the price of coffee increases (a normal good), which of the following is most likely to happen?

(A) An increase in the quantity of coffee consumers want to purchase

(B) No change in the quantity of coffee consumers want to purchase

(C) A decrease in the quantity of coffee consumers want to purchase

(D) An increase (shift)in the demand for coffee

(E) A decrease (shift)in the demand for coffee

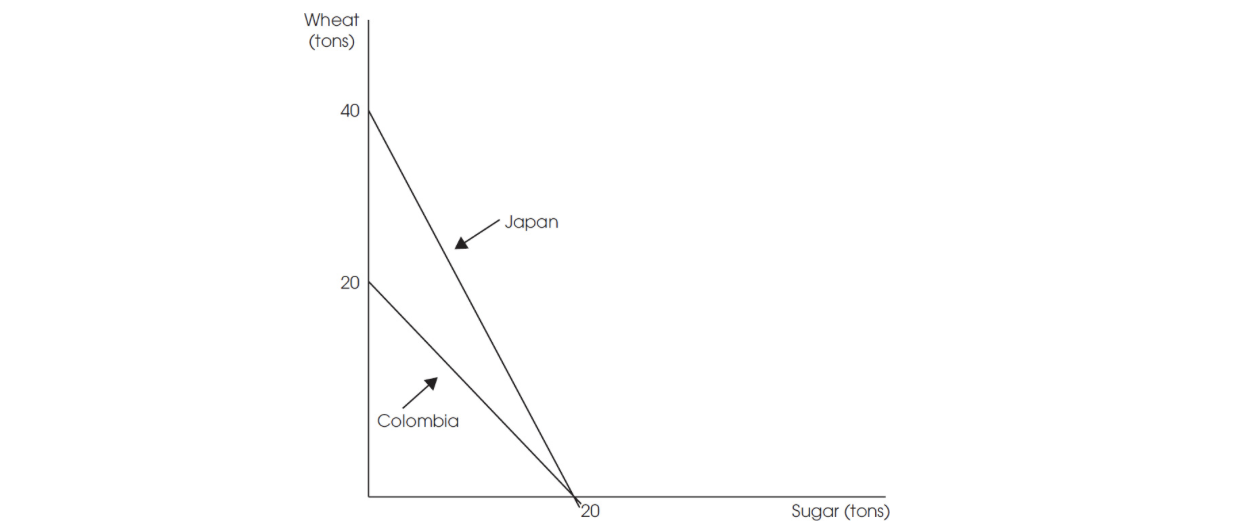

Use the following graph for Question 29.

29. The production possibilities graph shows how much each country can produce in a year. According to the graph, which of the following is true?

(A) Colombia has an absolute advantage in the production of wheat.

(B) Japan has a comparative advantage in the production of sugar.

(C) Colombia has a comparative advantage in the production of wheat.

(D) Japan cannot benefit from trade with Colombia.

(E) Japan has a comparative advantage in the production of wheat.

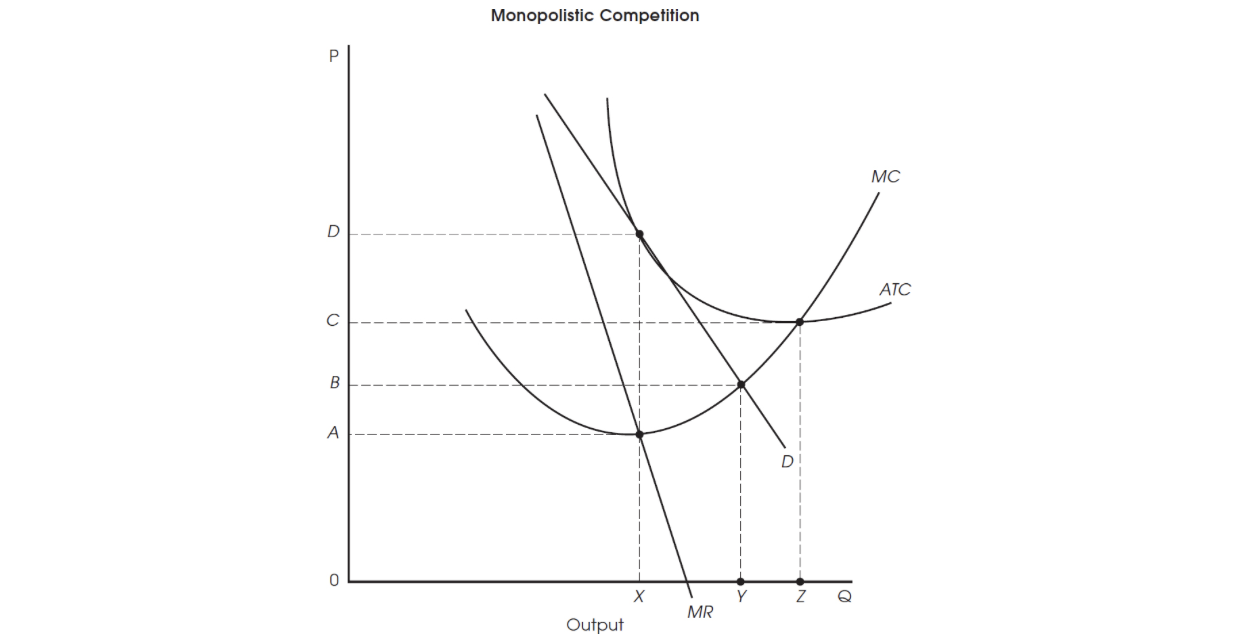

Questions 30–31 are based on the figure below.

30. For this firm operating under monopolistic competition, which of the following is the profit- maximizing output and price?

(A) OX output and OA price

(B) OX output and OD price

(C) OX output and OB price

(D) OZ output and OC price

(E) OZ output and OA price

31. At the profit-maximizing output, which of the following is correct?

(A) Economic profits are zero, and the firm is operating efficiently.

(B) Economic profits are above normal, and output is greater than under perfect competition.

(C) Economic losses are present.

(D) Price is less than marginal cost.

(E) Economic profits are zero, and the firm is operating inefficiently.

32. Which of the following best exemplifies economies of scale?

(A) As a firm’s output decreases, long-run average total cost decreases.

(B) As a firm’s output increases, long-run average total cost increases.

(C) As a firm’s output increases, long-run average total cost decreases.

(D) As a firm’s output increases, long-run average total cost remains constant.

(E) As a firm becomes larger, it becomes less productive.

33. Which of the following is correct?

(A) In the long run, all inputs are variable.

(B) In the short run, all inputs are variable.

(C) In the long run, supply is not able to adjust fully to changes in demand.

(D) In the short run, supply is able to adjust fully to changes in demand.

(E) A short run is any distance less than one mile.

34. If a firm decreases its prices by 15 percent and the quantity demanded increases by 30 percent, which of the following is correct?

(A) The price elasticity of demand is unit elastic.

(B) The price elasticity of demand is perfectly elastic.

(C) The price elasticity of demand is relatively elastic.

(D) The numerical coefficient of elasticity is equal to one.

(E) The numerical coefficient of elasticity is less than one.

35. At its current level of output, a firm uses two inputs in the production process, labor and robots. Robots produce an output of 1,000 units a day and cost $500, and labor produces 200 units a day and costs $100. In order to lower total production costs, how should the firm change its use of labor and robots?

(A) Increase both amounts of labor and robots.

(B) Use more robots and less labor.

(C) Use more labor and fewer robots.

(D) Use less labor and fewer robots.

(E) Maintain the current level of robots and labor.

36. When marginal cost equals price in a perfectly competitive product market in long-run equilibrium, which of the following is NOT true?

(A) There is allocative efficiency as price = marginal cost.

(B) There is productive efficiency as price = minimum average total cost.

(C) The perfectly competitive firm is earning economic profits.

(D) The market is producing the amount of goods desired by society.

(E) The firm is earning a normal profit.

37. Which of the following is a correct statement?

(A) Average total cost equals marginal cost plus average fixed costs.

(B) Average total cost equals marginal costs plus average variable costs.

(C) Average total cost equals average fixed costs plus average variable costs.

(D) Total fixed costs vary with output.

(E) Total fixed costs equal total variable costs at zero output.

38. Which of the following describes a monopolistically competitive market?

(A) A small number of firms with high barriers to entry and exit

(B) A large number of firms with high barriers to entry and exit

(C) A small number of firms and allocative efficiency

(D) It produces products with no close substitutes

(E) Low barriers to entry and exit and excess capacity

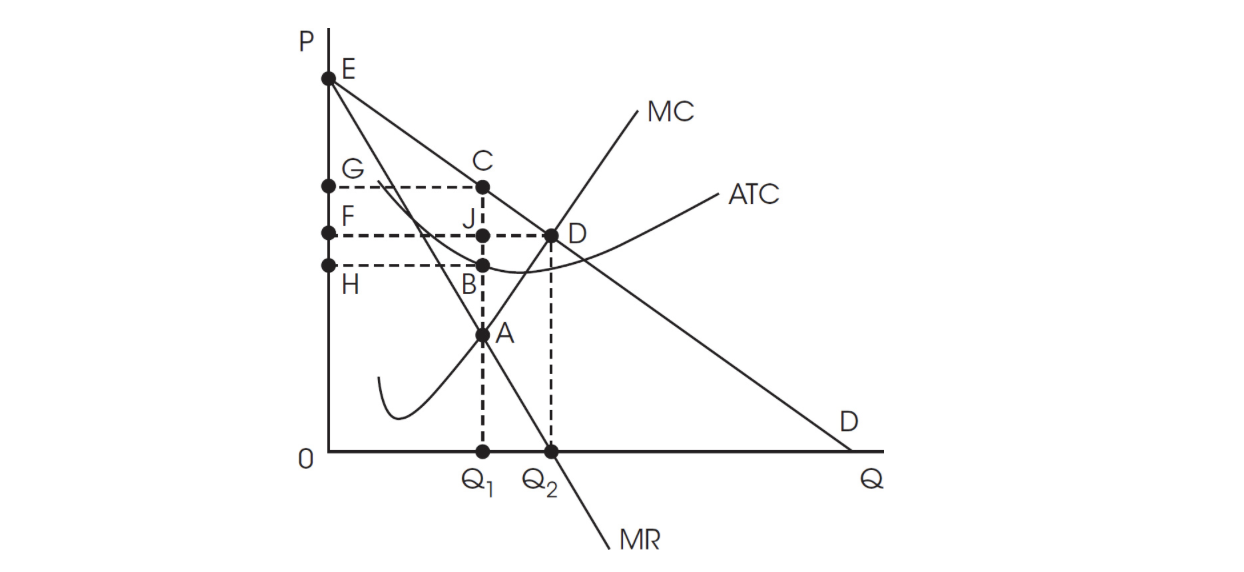

Questions 39–41 are based on this monopoly graph.

39. If this firm was producing at the socially optimal quantity, what area would be the consumer surplus?

(A) ECG

(B) CDA

(C) EDF

(D) GCBH

(E) GCJF

40. The deadweight loss as the result of the monopoly producing at the profit-maximizing quantity is the area of

(A) ECG

(B) CDA

(C) EDF

(D) GCBH

(E) GCJF

41. The consumer surplus of the monopoly producing at the profit-maximizing quantity is

(A) ECG

(B) CDA

(C) EDF

(D) GCBH

(E) GCJF

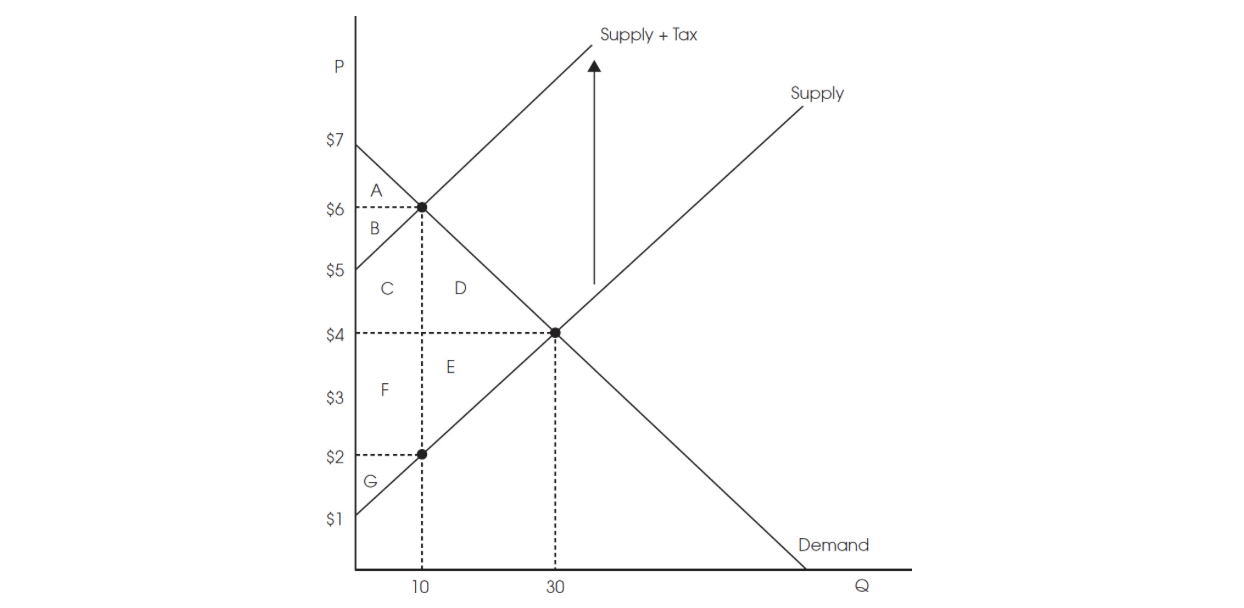

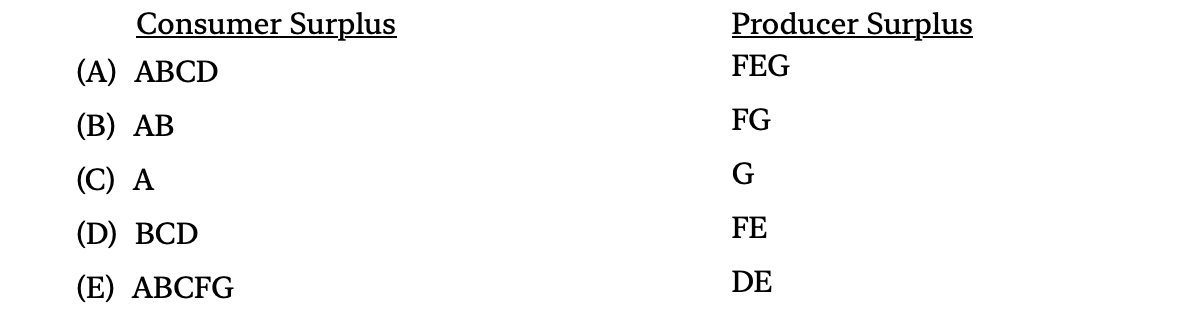

Use the following graph for Questions 42, 43, and 44.

42. The market shown in the graph has had a per-unit tax placed on its production. What are the after-tax consumer and producer surpluses?

42. The market shown in the graph has had a per-unit tax placed on its production. What are the after-tax consumer and producer surpluses?

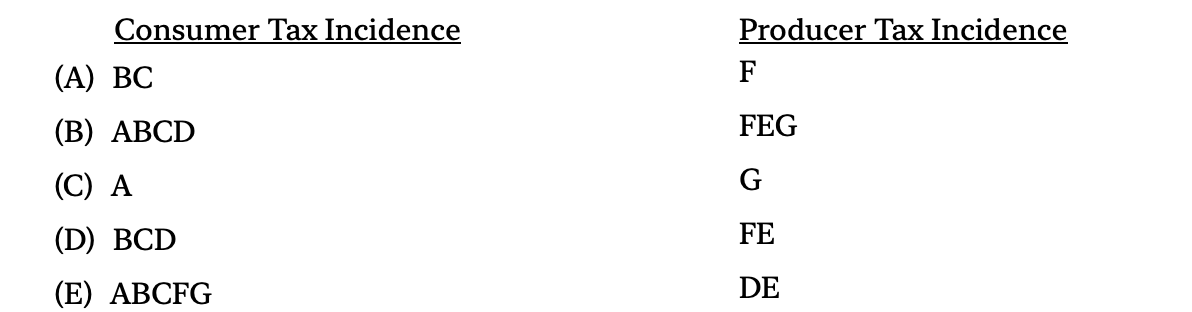

43. The market shown in the graph has had a per-unit tax placed on its production. What is the tax incidence, or burden of the tax paid by consumers and producers?

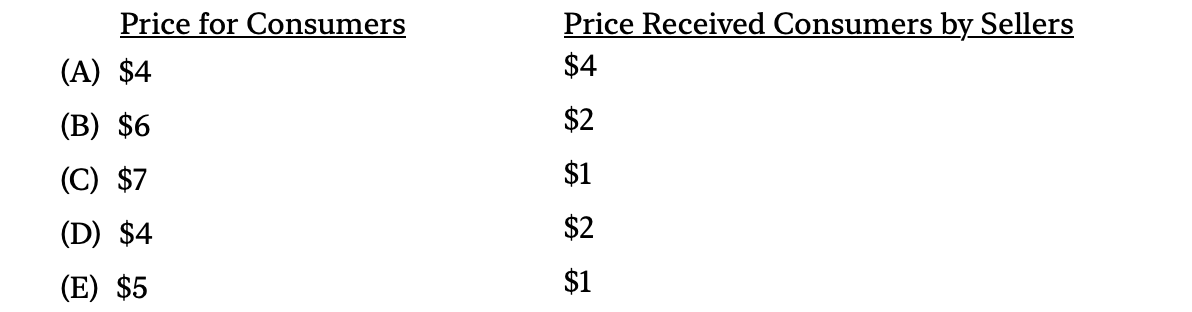

44.The market shown on the graph has had a per-unit tax placed on its production. What is the after-tax price paid by consumers and the after-tax price received by producers?

45. If, for each additional unit of a variable input added, the increases in output become smaller, which of the following correctly identifies the concept?

(A) Diminishing marginal returns

(B) Diminishing marginal utility

(C) Increasing marginal utility

(D) Increasing marginal productivity

(E) Constant costs

46. Which of the following is correct about the demand for labor?

(A) The demand for labor is independent of the demand for other inputs or resources.

(B) The demand for labor is independent of the demand for the products produced by labor.

(C) The demand for labor is independent of the availability of other inputs or resources.

(D) The demand for labor is derived from the demand for the products produced by labor.

(E) The demand for labor is derived from the demand for labor unions.

47. If an increase in the price of good Y causes the quantity demanded of good X to increase, this means the two goods are

(A) complementary goods.

(B) substitute goods.

(C) inferior goods.

(D) normal goods.

(E) independent goods.

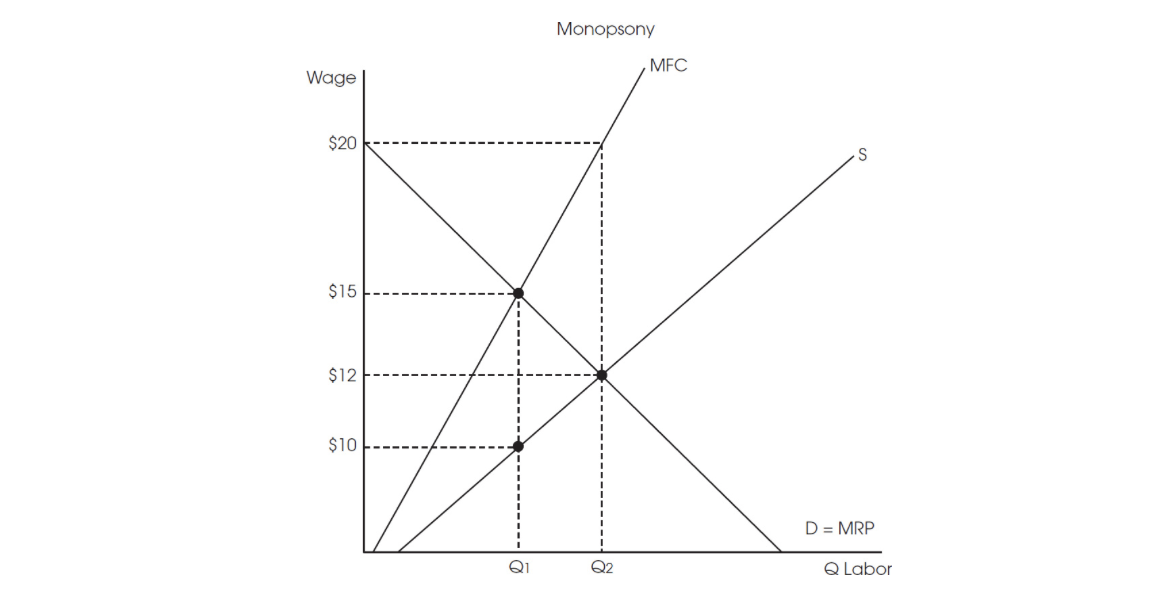

Use the following graph for Question 48.

48.The graph shows a monopsony labor market. What is the profit-maximizing wage and quantity of workers hired by the monopsonist?